You can certainly do very because of the deciding on the best home mortgage-the one that will not be as well risky to you personally

Lea Uradu, J.D. is actually a good Maryland Condition Entered Taxation Preparer, State Certified Notary Societal, Authoritative VITA Income tax Preparer, loans in Winfield Irs Yearly Submitting Season System Participant, and you may Taxation Publisher.

Skylar Clarine try a fact-examiner and you may expert inside personal fund having a selection of sense along with veterinarian technology and you may flick degree.

One of the greatest sessions the world discovered regarding subprime crisis off 2008 would be the fact we want to proceed that have caution whenever credit currency to find otherwise refinance a property. The type of mortgage you decide on can indicate the difference between owning your residence outright someday otherwise ending up regarding center out-of a property foreclosure if not case of bankruptcy many years for the the loan label.

Key Takeaways

- People financial was risky when it is matched into the incorrect brand of debtor.

- You’re going to be purchasing even more which have a 40-12 months fixed-speed mortgage, even from the a lower life expectancy speed.

- Adjustable-rates home loan interest rates can go up, definition it is possible to shell out a lot more after they reset.

- Interest-just home loan prices was more than other people and you will have to spend the money for prominent off of the a specific go out.

- Interest-merely adjustable-rates mortgages combine a couple high-risk issues into the one.

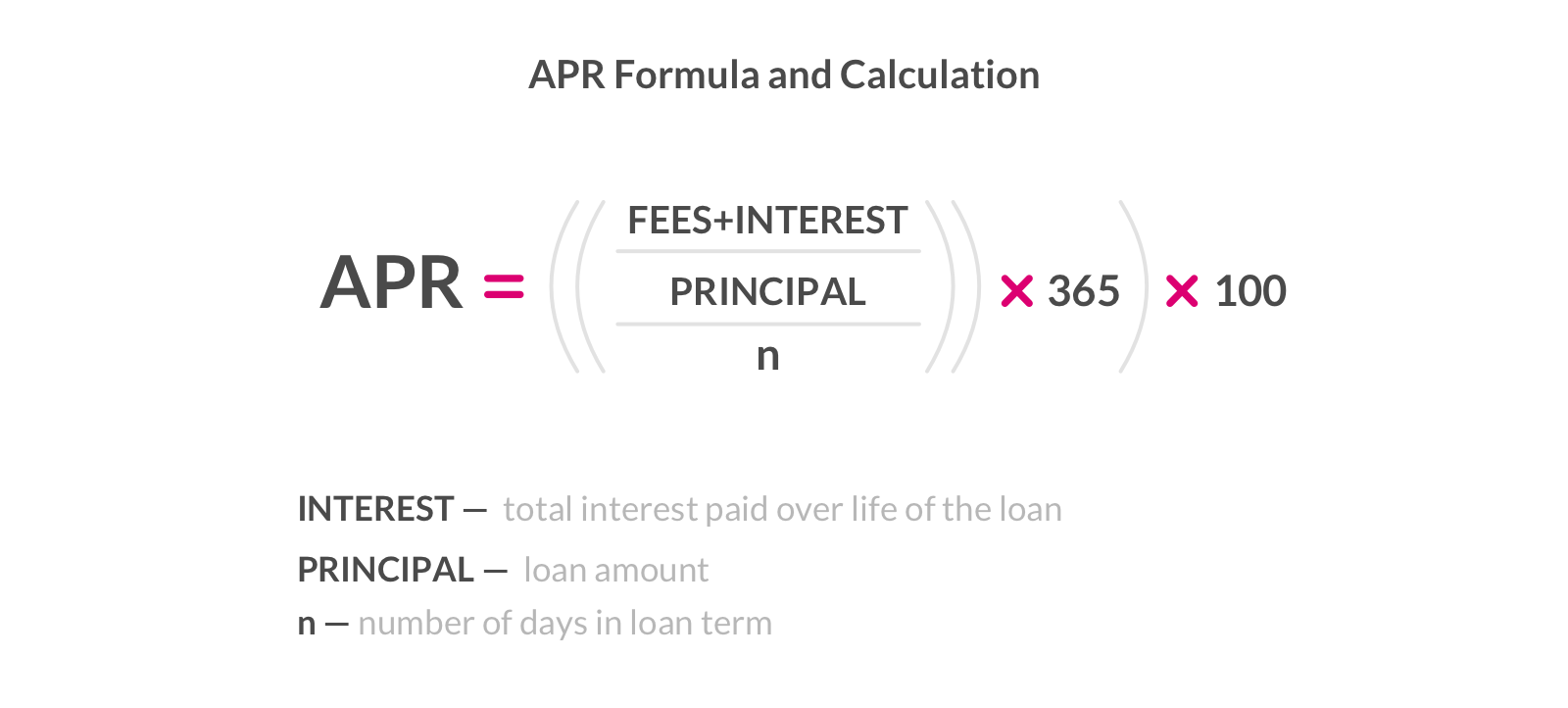

Why are a home loan High-risk?

Most of us have come to believe any particular one brand of mortgages are inherently risky due to what happened in the property drama. In fact, a few of the mortgage loans in the marketplace just weren’t particularly risky for the ideal consumers.

Within the 2008, specific mortgage brands had been are matched to your completely wrong individuals, and you can lenders was indeed drawing them inside towards possibility of refinancing in the near future. This could have has worked when home prices was in fact ascending, not whenever home prices reach miss.

40-Year Repaired-Price Mortgage loans

Consumers having repaired-price mortgages try not to live with uncertainty, however, that doesn’t mean this type of mortgages will always be sensible. That’s because you get spending significantly more finally. The new offered the borrowing from the bank several months, more interest you get spending.

We have found good hypothetical disease. Can you imagine you want to pick an effective $200,000 home with good 10% advance payment. The quantity you will need to borrow is actually $180,000 ($2 hundred,000 without $20,000). From the an interest rate of five%, here you will find the monthly payments plus the total matter possible spend towards the domestic significantly less than various conditions for folks who hold the financing for its lives:

When you never re-finance and sustain the loan as it is, you are able to shell out $236, in focus by yourself by the end of the forty-season months. This is a basic assessment. The pace will probably be lower to the 15-season mortgage additionally the higher for the 40-12 months mortgage.

As you can tell about 2nd chart, the latest 40-seasons financial is actually 0.6% higher in the focus than the 29-12 months home loan. One lowers their payment because of the simply $ thirty days, away from $ to help you $ Yet not, you will be charged your an impressive $107, more over the life span of your loan.

That’s a large amount of cash which will check out money your retirement or even to purchase your own youngsters’ degree. At best, you are forgoing currency that you might possess used on holidays, renovations, and any other costs.

Adjustable-Price Mortgage loans (ARMs)

Adjustable-rates mortgages (ARMs) enjoys a predetermined rate of interest to possess a primary title anywhere between 6 months to a decade. That it initially interest rate, possibly entitled an intro rate, might be below the interest rate on the an effective 15- or 30-season fixed mortgage. Following the initial title, the rate adjusts periodically. Then it one per year, once twice yearly, or even monthly.